The SECURE Act is now in effect.

For retirees as well as those close to retirement, there might only be small changes. Maybe one exception

For those with a decade or two or more before retirement, depending on your individual situation, SECURE could have more impact. If you are primarily in the "gig" economy, you might now qualify for a 401-k that you didn't qualify before. In itself that could be significant. If you turn out to be able to take advantage of a nice match to some or all of contributions you make, then even better for you.

The potential positive exception for those close to retirement is if your own 401-k makes an annuity inside your 401-k available to you AND that annuity turns out to be significantly better for you. Hypothetically that might be possible, but we have not seen actual situations yet.

Some key parts:

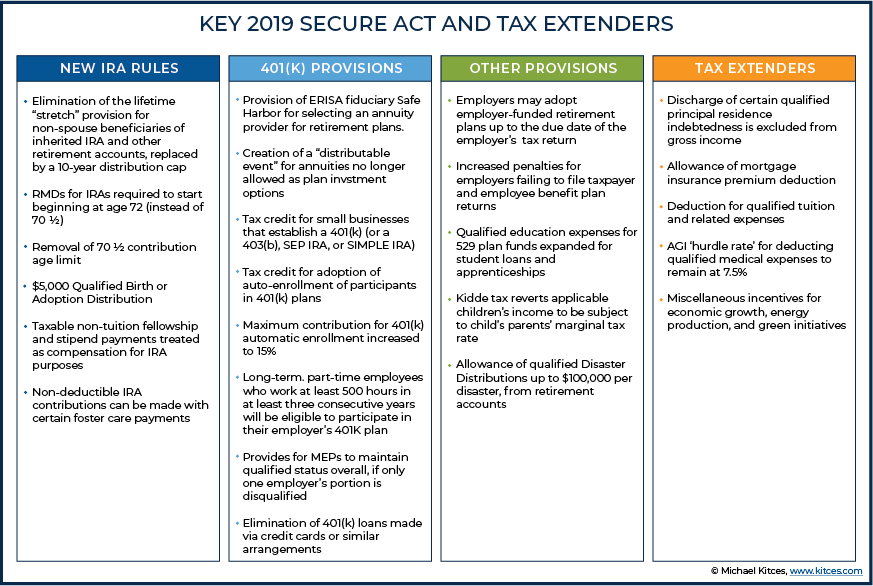

- Make it easier for small businesses to set up 401(k)s by increasing the cap under which they can automatically enroll workers in “safe harbor” retirement plans, from 10% of wages to 15%

. - Provide a maximum tax credit of $500 per year to employers who create a 401(k) or SIMPLE IRA plan with automatic enrollment.

- Enable businesses to sign up part-time employees who work either 1,000 hours throughout the year or have three consecutive years with 500 hours of service.

- Encourage plan sponsors to include annuities as an option in workplace plans by reducing their liability if the insurer cannot meet its financial obligations.

- Encourage employers to include more annuities in 401(k) plans by removing their fear of legal liability if the annuity provider fails to provide and also not requiring them to choose the lowest-cost plan. (This could be something of a double-edged sword. Employees will need to look extra-carefully as these

- Push back the age at which retirement plan participants need to take required minimum distributions (RMDs), from 70½ to 72, for those who are not 70½ by the end of 2019.

- Removal of a provision known as the stretch IRA, which has allowed non-spouses inheriting retirement accounts to stretch out disbursements over their lifetimes. The new rules will require a full payout from the inherited IRA within 10 years of the death of the original account holder, raising an estimated $15.7 billion in additional tax revenue.

- Allow the use of tax-advantaged 529 accounts for qualified student loan repayments (up to $10,000 annually).

- Permit penalty-free withdrawals of $5,000 from 401(k) accounts to defray the costs of having or adopting a child.